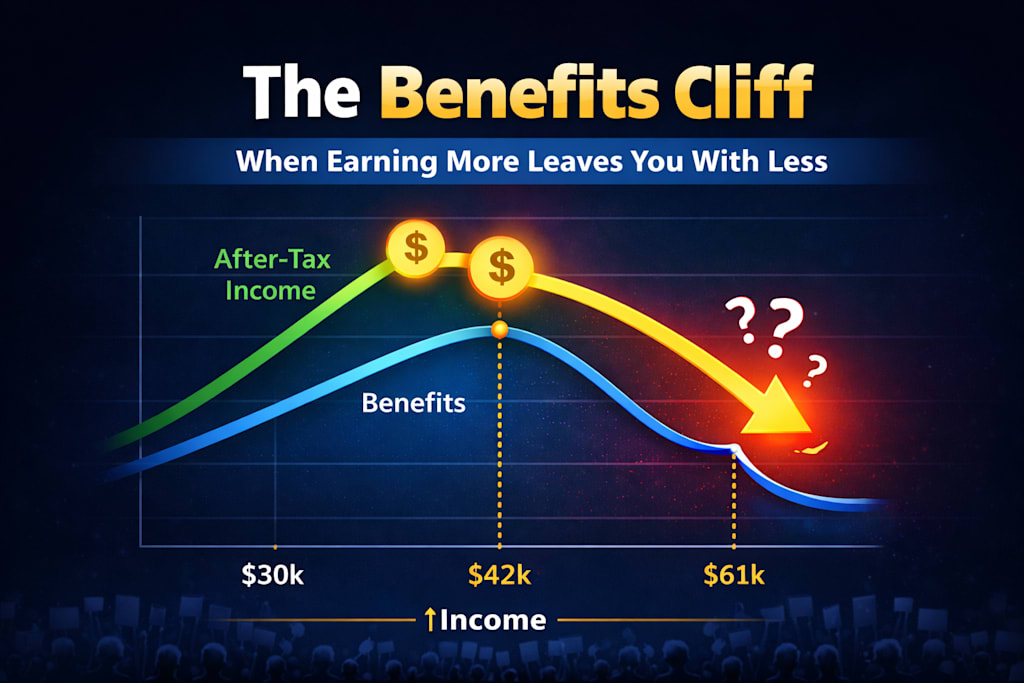

The "Benefits Cliff"

When Earning More Leaves You With Less

The System Is Not Cash, It Is Replacement

For a family of five in Salem, Oregon, the low-income support system is not built primarily on direct cash transfers. It is built on a small number of high-impact programs that function as after-tax purchasing power, replacing major expenses rather than adding to pre-tax income. This distinction matters because it changes how the system must be evaluated. Income is taxed before it becomes usable, while benefits replace costs that would otherwise require after-tax dollars. That means these programs effectively operate as a parallel income structure, but one that is locked into specific categories such as food, housing, childcare, and healthcare rather than flexible cash.

The primary components of this system include SNAP for food, housing assistance tied to income thresholds, ERDC childcare support, Oregon Health Plan coverage, and smaller forms of utility assistance. When stacked together, these programs can represent a substantial portion of a household’s total usable resources. SNAP alone can provide up to $1,183 per month for a family of five. Housing assistance can reduce rent obligations by thousands annually by limiting the tenant share to roughly 30% of income. Childcare support through ERDC can replace tens of thousands of dollars in expenses depending on need. Healthcare coverage eliminates premiums and significantly reduces exposure to large medical costs. These are not theoretical benefits. They directly replace expenses that must otherwise be paid with earned income after taxes.

What the Stack Actually Looks Like

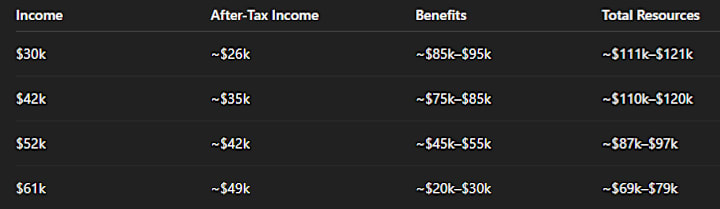

When these programs are combined at very low income levels, the total value becomes substantial. Available program data shows that a realistic combined value for these supports can reach roughly $85,000 to $95,000 per year in replaced or subsidized expenses when including childcare, housing, food, healthcare, and disability-related supports where applicable. When paired with a modest earned income, such as $30,000 annually, the household may have around $26,000 in after-tax income plus these benefits, resulting in total usable resources in the range of approximately $111,000 to $121,000.

However, nearly all of these resources are tied to immediate necessities. Food benefits cannot be converted into savings. Housing subsidies cannot be liquidated into equity. Childcare assistance replaces a required cost of working rather than generating surplus. Healthcare coverage reduces risk and cost but does not build assets. This means that while total usable resources can be high, discretionary cash remains limited. The system sustains stability in the present but does little to enable long-term wealth-building. Families may find themselves unable to accumulate savings, invest, or move into asset ownership despite having a relatively high level of total support.

Wealth Building Is Structurally Constrained

While the total value of support at lower income levels can appear high when measured as replaced expenses, very little of it contributes to long-term financial stability or asset accumulation. These benefits are largely restricted to immediate consumption needs such as food, rent, childcare, and healthcare, and cannot be converted into savings, investment capital, or ownership. As a result, households may have relatively high total usable resources but still lack the ability to build retirement savings, contribute meaningfully to employer-sponsored plans such as a 401(k), purchase bonds or other appreciating assets, or accumulate capital for homeownership.

Because eligibility for many programs is tied to income and, in some cases, asset thresholds, increases in earnings or savings can accelerate the loss of benefits. This creates a structural constraint on upward mobility within certain income ranges. The system can stabilize short-term living conditions while limiting the mechanisms that typically lead to long-term financial independence. In this way, the structure can reinforce continued reliance on support rather than facilitating a transition toward self-sustaining financial growth.

The Cliff Is Created by Overlapping Phaseouts

The structure of the system is not coordinated. Each program has its own eligibility thresholds and phaseout rules. SNAP declines with income and phases out within its eligibility range. Housing assistance is tied to area median income limits and ends when income exceeds those thresholds. Adult healthcare eligibility through OHP is limited to lower income levels, though extended coverage can apply in higher bands. ERDC childcare support tapers gradually rather than ending abruptly, but its value decreases as required copays increase. Utility assistance follows its own income-based criteria and is often linked to eligibility for other programs.

The critical issue is that these programs do not phase out independently across widely separated income ranges. Instead, they cluster within a relatively narrow band. As income rises into approximately the $42,000 to $61,000 range for a family of five, multiple programs begin to reduce or terminate simultaneously. This creates a structural compression point where several large sources of support are lost at the same time. Because these benefits represent real usable value, their loss is not equivalent to losing pre-tax income. Replacing them requires earning significantly more than their nominal value due to taxation.

This effect becomes clearer when total usable resources are compared across income levels:

When Earning More Produces Less

Because income is taxed before it becomes usable, replacing lost benefits requires more than one dollar of gross income for every dollar of benefit lost. In practical terms, replacing one dollar of benefits may require approximately $1.25 to $1.40 in gross earnings depending on tax rates. This creates an immediate mismatch between what is lost and what must be earned to replace it, even before considering how multiple programs phase out at the same time.

When benefit losses occur across several programs simultaneously, the required income increase to offset those losses can far exceed the actual increase in wages. As income rises within this range, after-tax earnings increase gradually, but the reduction in benefits can occur more quickly. The result is a defined income band in which marginal earnings produce little net gain or even a net loss in total usable resources, despite higher gross income.

Not Every Family Receives Everything, But the Pattern Still Holds

It is important to note that not all households receive the full stack of benefits at the same time. Housing assistance is often limited by waitlists and availability. Childcare support depends on provider access and eligibility conditions. Other programs require separate applications and may not be utilized even when a household qualifies. These systems operate independently and do not coordinate with one another.

Despite this, they share similar income-based thresholds tied to federal poverty levels and area median income calculations. This means that even when a household does not receive every available benefit, it can still encounter overlapping reductions as income rises. The effect does not depend on perfect stacking. It emerges from the alignment of eligibility thresholds across separate programs. For many households, this still results in a sharp reduction in total support within a relatively narrow income range.

The Costs That Do Not Show Up on Paper

The financial effects are only part of the picture. As households move out of eligibility ranges, they often need to increase working hours or take on additional employment to compensate for lost support. This reduces the time available for parenting, increases reliance on external childcare, and places additional strain on household routines. The ability to maintain an organized home, prepare meals, and manage daily responsibilities can decline as time becomes more limited.

These pressures extend into relationships. Reduced time together, increased fatigue, and the stress of financial instability can affect the quality of family life. These are not abstract concerns. They are direct consequences of the transition from supported income levels to higher earnings within a system that removes support faster than income grows. These costs do not appear in financial calculations, but they are real and significant.

The Structural Outcome

The system is capable of delivering a high level of total support at very low income levels, but it does so in a way that is tied to specific categories of spending and constrained by eligibility thresholds. As income increases, the loss of these supports occurs in overlapping bands, creating a benefits cliff where total usable resources can decline even as earnings rise. At the same time, the structure limits the ability to build long-term assets by restricting resources to immediate needs.

The result is a system that stabilizes households at lower income levels but creates a difficult transition zone where incremental progress can be penalized. Meaningful improvement in total resources typically requires moving well beyond this range, to an income level high enough to replace both the lost benefits and the taxes applied to new earnings. Until that point, households can find themselves in a position where earning more does not immediately lead to greater financial stability.

About the Creator

Peter Thwing - Host of the FST Podcast

Peter unites intellect, wisdom, curiosity, and empathy —

Writing at the crossroads of faith, philosophy, and freedom —

Confronting confusion with clarity —

Guiding readers toward courage, conviction, and renewal —

With love, grace, and truth.

Keep reading

More stories from Peter Thwing - Host of the FST Podcast and writers in The Swamp and other communities.

The Protection-of-Innocence Reciprocity Doctrine

Core Moral Premise The highest duty of any legitimate social order is the protection of innocent life. Innocent life has absolute moral primacy. Any system that systematically insulates predators, tolerates predatory asymmetry, rewards hypocrisy, or allows aggressors to retain insulation has inverted its purpose and forfeited legitimacy. Truth, justice, reciprocity, humility, mercy, forgiveness, and vertical accountability are structural necessities rather than optional virtues. Vertical accountability means recognition of and submission to a moral law higher than oneself. Authority must flow toward those who most consistently demonstrate sustained competence in moral and epistemic discipline. This competence is shown through observable conduct and trajectory over time, not through doctrinal label, tribal identity, credential alone, or self-profession.

By Peter Thwing - Host of the FST Podcastabout a month ago in The Swamp

The Forsyth House Fire

Since 1851, Forsyth House has stood on the corner of Union Street and Gordon Street in the heart of Glasgow. Its iconic, or was... because on Sunday 8th of March, 2026, a fire broke out in a small, seemingly un-named shop in the building and tore all that history down. As I write, the rubble is still unsettled and the street is still blocked off. Central Station is quiet on the upper level, and around 30 small businesses have quite literally gone up in smoke.

By S. A. Crawford23 days ago in The Swamp

The Ecosystem

Why Swamps Are the Planet's Most Important and Most Misunderstood Landscape THE WORLD'S MOST HATED ECOSYSTEM 🐊 For centuries human civilization has treated swamps, marshes, bogs, and wetlands as wastelands, as obstacles to progress that should be drained, filled, developed, and converted into productive land, and this attitude has resulted in the destruction of approximately sixty-four percent of the world's wetlands since 1900 with the rate of loss accelerating in recent decades despite growing scientific understanding that wetlands are not wastelands but rather among the most ecologically valuable and productive ecosystems on Earth, providing services worth an estimated forty-seven trillion dollars annually including water purification, flood protection, carbon sequestration, biodiversity support, and coastal storm buffering that no human technology can replicate at comparable scale or cost, and the continuing destruction of these ecosystems represents one of the most catastrophic environmental miscalculations in human history driven by the fundamental misunderstanding that an ecosystem's value is determined by its utility for agriculture or development rather than by its ecological function 🌍

By The Curious Writerabout 16 hours ago in The Swamp

Comments

There are no comments for this story

Be the first to respond and start the conversation.