Europe’s Fixed Wireless Access Boom Is Reshaping the Future of Broadband

As fiber rollout challenges persist, Europe’s Fixed Wireless Access market is emerging as a faster, more flexible solution for homes, businesses, and underserved communities.

Reliable internet is no longer a luxury in Europe—it is the backbone of work, education, entertainment, commerce, and public services. Yet despite years of investment in fiber and cable networks, millions of homes and businesses across the continent still face broadband limitations, especially in rural and semi-urban areas. That gap is exactly where Fixed Wireless Access, better known as FWA, is beginning to change the story.

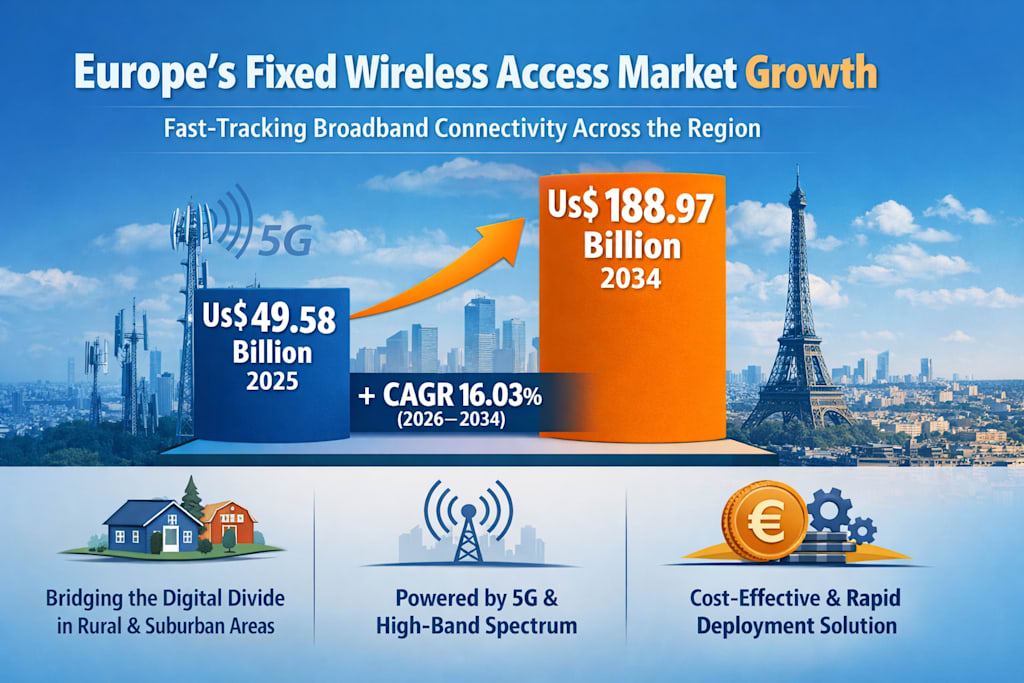

According to Renub Research data shared in your source material, the Europe Fixed Wireless Access Market is projected to rise from US$ 49.58 Billion in 2025 to US$ 188.97 Billion by 2034, expanding at a CAGR of 16.03% from 2026 to 2034. Those numbers point to more than just telecom growth—they reflect a structural shift in how Europe may deliver broadband in the next decade.

In simple terms, FWA uses wireless networks—typically 4G, 5G, or higher-frequency radio bands—to provide internet to homes and businesses without relying entirely on underground fiber or copper cables. Instead of waiting months or even years for trenching and physical network expansion, users can often receive broadband through a receiver installed at the premises, connected to a nearby base station. That deployment speed is one of the strongest reasons why FWA is moving from a niche option into a serious broadband contender.

Europe’s digital ambitions are high. Governments want universal connectivity, businesses need resilient internet infrastructure, and households expect streaming, gaming, video conferencing, and cloud services to work without interruption. Fiber remains the gold standard in many places, but it is not always the fastest or most cost-effective route to coverage. In that context, FWA is no longer just an alternative—it is becoming a strategic necessity.

One of the biggest forces behind this market expansion is the rising broadband demand in underserved and suburban regions. Europe is a patchwork of dense urban centers, small towns, villages, mountain communities, coastal settlements, and outer suburban zones. Extending fiber into every last-mile location can be technically difficult and financially inefficient. FWA helps telecom operators bypass those bottlenecks by delivering internet over the air instead of through costly ground infrastructure.

This matters especially for households that are stuck with outdated ADSL or low-performance cable connections. It also matters for small businesses in areas where digital competitiveness depends on reliable internet but where infrastructure upgrades tend to arrive late. For many of these users, FWA becomes the quickest path to better speeds and more stable service.

The timing also aligns perfectly with the rapid expansion of 5G networks across Europe. As telecom operators continue building 5G infrastructure, they are discovering that the same investments made for mobile connectivity can also support fixed broadband services. That creates a powerful business case. Rather than building entirely separate systems for home internet, providers can reuse parts of their mobile radio access network to offer FWA packages with competitive speeds and service quality.

This is where 5G becomes more than a smartphone story.

With technologies such as Massive MIMO, beamforming, and carrier aggregation, 5G-enabled FWA can offer significantly better capacity and lower latency than earlier wireless generations. Mid-band and high-band spectrum, including 24–39 GHz ranges, are opening the door to faster and more stable fixed wireless services. That means users in select areas can access broadband experiences that increasingly rival wired alternatives, especially for video streaming, remote work, online learning, and cloud-based productivity.

For telecom companies, the economics are equally attractive. Rolling out fiber across difficult terrain, older neighborhoods, or remote communities can involve enormous capital expenditure, long regulatory approvals, and disruptive civil works. FWA avoids much of that burden. It requires fewer permits, less excavation, and quicker customer onboarding. That translates into faster time-to-revenue.

And in telecom, speed to monetization matters.

Instead of waiting years for infrastructure returns, operators can launch service in a new region much faster, test demand, and scale gradually. That flexibility is particularly appealing for regional internet providers, mobile network operators, and even smaller challenger brands looking to compete with larger incumbents. FWA allows them to use existing assets more efficiently while also aligning with national broadband targets.

This flexibility is helping FWA gain traction in both consumer and commercial markets. On the residential side, households increasingly expect broadband that can support multiple devices, high-definition streaming, online gaming, smart home tools, and hybrid work setups. FWA is well positioned to meet those expectations, particularly in locations where fiber remains unavailable or delayed.

On the business side, the value proposition becomes even more compelling.

For small and medium-sized enterprises, FWA offers a practical way to secure fast broadband without waiting for long installation cycles. For larger organizations, it can act as either a primary connection or a backup line to improve resilience. In sectors such as retail, logistics, hospitality, and temporary events, the ability to deploy connectivity quickly can make a real operational difference. Businesses are not just buying bandwidth—they are buying speed, uptime, and business continuity.

The commercial opportunity is especially strong in Europe’s growing digital economy, where cloud software, remote access systems, payment infrastructure, surveillance, and communications platforms all depend on stable internet. In that sense, FWA is not only solving connectivity problems; it is supporting productivity and business modernization across multiple industries.

Still, the market is not without obstacles.

One major challenge is regulatory fragmentation. Europe may be economically integrated in many respects, but telecom regulation and spectrum allocation are still handled differently from country to country. Licensing frameworks, channel availability, power restrictions, and deployment rules can vary significantly. That creates complications for vendors and operators trying to scale services across multiple markets.

A company that wants to offer FWA solutions in Germany, France, the UK, Italy, or the Netherlands may face different equipment requirements, certification standards, and spectrum strategies in each country. This patchwork raises operational complexity and can slow deployment.

Another challenge lies in the technical limitations of higher-frequency wireless bands. While mmWave and similar high-band technologies can offer very high speeds, they also struggle more with range, building penetration, foliage, rain fade, and line-of-sight issues. In dense urban environments, signal interference and physical obstructions can affect performance. In rural settings, long distances and obstacles may require stronger antennas or more infrastructure than initially expected.

This is why FWA should not be viewed as a universal replacement for fiber. It works best as part of a broader connectivity strategy—one that blends fiber, wireless, and hybrid approaches based on geography, economics, and user demand.

That balanced strategy is already visible in several European countries.

Germany, for instance, represents a particularly promising market because of its large geography, ambitious broadband goals, and mixed urban-rural infrastructure realities. Fiber and cable remain strong in some urban areas, but suburban and rural communities continue to offer room for wireless broadband expansion. The country’s regulatory focus on connectivity and coverage also creates an environment where FWA can play a significant role. According to the provided source material, network activity and operator partnerships are already reinforcing this direction.

The United Kingdom also stands out as a dynamic FWA market. Rural connectivity remains a pressing issue in parts of the UK, and wireless broadband has become a practical complement to fixed-line deployment. The market is also benefiting from competition, policy support, and demand from consumers who prioritize speed and convenience over waiting for infrastructure projects to reach their location.

Meanwhile, the Netherlands presents a different but equally interesting use case. Because fiber penetration is already strong in many urban areas, FWA there often targets niche or flexible applications—such as industrial parks, temporary connectivity, construction sites, and business-specific deployments. In a digitally mature environment, FWA is not always replacing fiber; sometimes it is filling the gaps fiber does not efficiently cover.

Another major area of momentum lies in the hardware ecosystem supporting FWA growth. Demand is increasing for advanced customer premises equipment (CPE), outdoor receivers, antennas, gateways, and multiband devices capable of handling both 4G and 5G. Operators want hardware that is easy to install, weather-resistant, software-upgradable, and compatible across different spectrum environments.

This is also pushing innovation among telecom vendors and equipment makers. Compact outdoor units, self-installation kits, virtualized network hardware, and edge-enabled devices are all becoming part of the broader FWA value chain. In short, this is not just a network story—it is also a device and infrastructure story.

And that matters because broadband competition in Europe is entering a more agile phase.

For years, the broadband race was framed mainly around who could lay the most fiber, fastest. That is still important. But now, the market is broadening. Operators are being forced to think not only about maximum speed, but also about deployment efficiency, geographic reach, service reliability, and return on infrastructure investment. FWA gives them a way to respond to all four.

That is why Europe’s Fixed Wireless Access market is not merely growing—it is becoming strategically important.

As digital transformation accelerates, broadband is increasingly tied to social equity, regional development, business competitiveness, and national resilience. A student in a remote town, a freelancer in a suburban apartment, a retailer in a growing edge-of-city district, and a logistics warehouse in an industrial corridor all rely on connectivity to participate fully in the modern economy. FWA helps bring those users into the fold faster.

Its real power lies in that practicality.

It does not need to defeat fiber to succeed. It only needs to solve broadband problems faster, more flexibly, and more affordably where traditional rollout models fall short. And in a continent as diverse and infrastructure-challenged as Europe, that is a very powerful proposition.

Final Thoughts

Europe’s broadband future will not be built by a single technology alone. Fiber will continue to lead in many high-capacity markets, but Fixed Wireless Access is proving that wireless broadband can no longer be treated as secondary. It is becoming a frontline solution for digital inclusion, commercial connectivity, and network expansion.

With the market expected to climb from US$ 49.58 Billion in 2025 to US$ 188.97 Billion by 2034, FWA is clearly moving into a much larger role in Europe’s telecom landscape. For operators, policymakers, investors, and consumers alike, this is a market worth watching closely.

About the Creator

Stanislav Kondrashov on Dubai’s Emergence as a Key Financial Center

Over the past decades, Dubai has transformed from a regional hub into a globally recognized financial center, characterized by connectivity, adaptability, and strategic positioning. This transformation did not occur by chance. It reflects a deliberate alignment of infrastructure, institutional frameworks, and international orientation. According to Stanislav Kondrashov, the rise of Dubai as a financial center offers valuable insight into how modern financial ecosystems are built and sustained.

By Stanislav Kondrashovabout 14 hours ago in Trader

Aura Energy Limited: Company Insights, Uranium Outlook, and Market Perspective

Introduction Aura Energy Limited is a resource-focused company operating in the global energy sector, with a strong emphasis on uranium exploration and development. As the demand for cleaner and more sustainable energy increases, companies like Aura Energy Limited are gaining attention from investors worldwide.

By Hammad Nawaz4 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.